Many businesses pay out money they don’t have to, such as paying a supplier twice. They might be small amounts individually, but amount to a substantial loss of cash in the aggregate. An accounts payable audit makes it easy to claw such cash back.

Paperless supplier invoices are already a fact of life, and e-billing is making great strides. The quest for operational efficiency and the need for compliance are driving businesses to adopt electronic invoicing. However, at this point, while the proportion of businesses using a paperless supplier invoicing solution is growing constantly, we are seeing many accounting irregularities continue to slip through the net. These changes are not eradicating the risk of error, making appropriate checks all the more necessary.

“Typically, such errors relate to over-payment. The most common are the result of double payments to suppliers or overlooked input VAT,” explains Alban Delsol, Managing Director Revenue at Runview, France’s leading firm in Profit Recovery and accounting records data mining.

Identifying residual errors

The internal and external audits run by businesses will find most errors in a system, but a residual level of errors will always escape their attention.

In terms of supplier over-payments, there are several possible sources:

- Double payment resulting from identical duplicate entries in the accounting system. “Surprising though it might seem, this is the type of error we see most often,” Alban Delsol reports;

- Double payment resulting from slightly different duplicate entries (a different invoice number or date, for example);

- Payment of the same invoice to the wrong party, then to the right one;

- Credit notes recorded as invoices;

- Down payments or installments paid overlooked when calculating the balance due;

- Currency conversion errors;

- etc.

Errors related to overlooked input VAT (value-added tax, a type of sales tax common in Europe, which businesses are permitted to claim back), meanwhile, fall into two categories:

- One-time errors related to incomplete or complicated invoices, or an unusual slip-up in the Procure-to-Pay process;

- Errors of a more recurrent nature arising from specific tax situations of which the accounting people are not necessarily aware. “In this category, we find errors in VAT treatment in relation to vehicles,” Delsol explains.

The amounts involved in supplier overpayments are often less than €5,000, and the recurring overlooked input VAT errors might individually be little more than loose change. But cumulatively, they can amount to substantial financial losses. “An accounts payable audit is intended to identify these residual errors and then recover the amounts involved,” Alban Delsol points out.

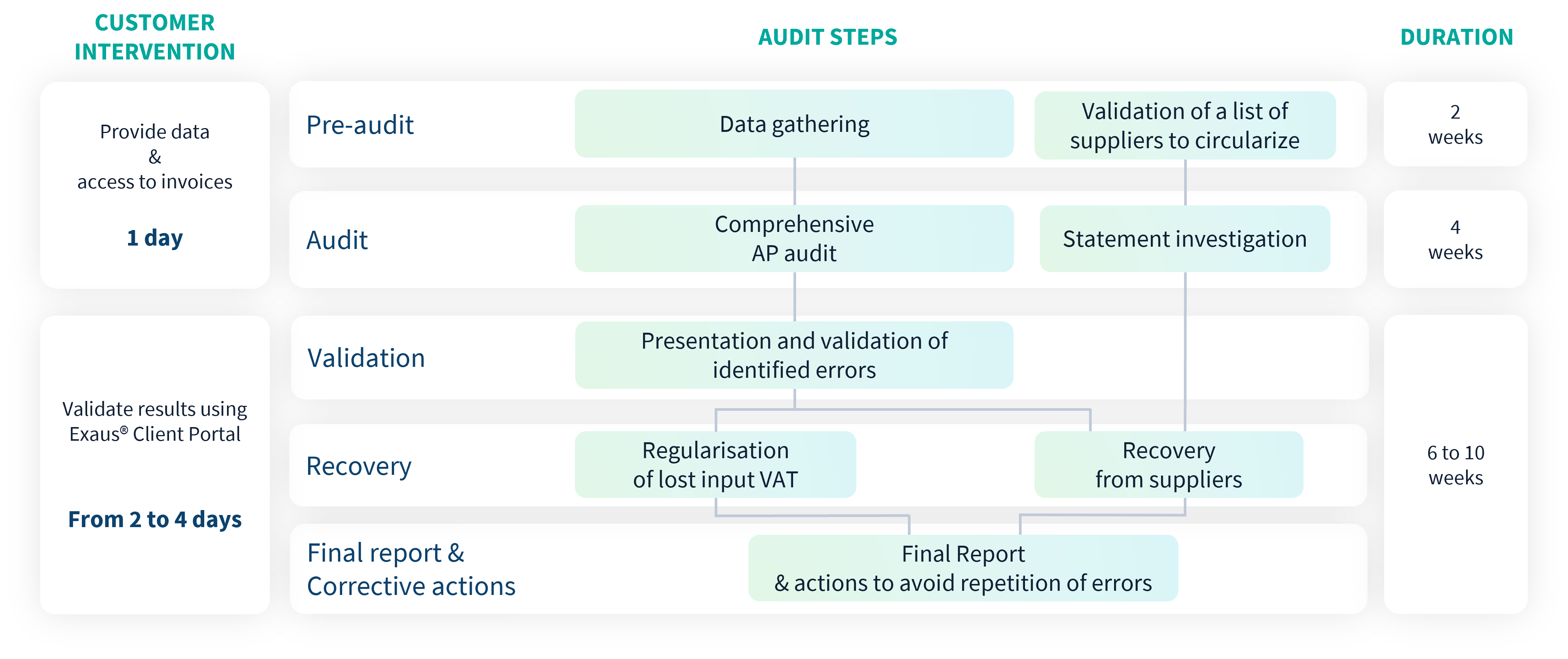

The main stages in a Profit Recovery audit

An accounts payable audit is usually run over two or three stages, generally taking two, maybe three, months.

Firstly, the accounting records are analyzed by purpose-built software. “Our consultants then usually visit the client to reconcile the computerized audit with the accounting documents, to fine-tune their findings,” continues Delsol.

Once the supporting documentation has been found, the client’s accounts department ratifies (or otherwise) the errors detected. “The client is always in control, and it is the client that decides whether to continue with the procedure,” Delsol stresses.

If they do, Runview moves to stage three, collecting money from the suppliers. This phase can take four to eight weeks.

Improving cash flow and processes

Whether data entry operations are managed in-house or by a shared services center, profit recovery offers many advantages.

The main benefit is the recovery of money previously lost, potentially amounting to tens of thousands for a mid-sized firm. Seven-figure sums have been recovered by larger corporations. And there is no risk whatsoever for the business, as profit recovery fees are usually proportional to the money recovered.

Besides the extra cash, an accounts payable audit also gives a business a fresh, outside perspective on all of its accounting procedures. “At the end of the audit, we give the client a report, with a cross-referenced examination of all the errors and their causes, together with some suggested areas for improvement,” Alban Delsol concludes. “After identifying and recovering more than €1.5m for a major name on France’s CAC40 index, our consultants examined the reliability of the procure-to-pay process it had in place, and showed how the rate of double payments was 10 times higher for invoices handled outside that process.”

About the author